Real estate investing and stocks are 2 major asset classes you’ll be looking at when reviewing your investment portfolio.

The oft-advised strategy is to diversify your investment in both real estate and stocks.

This advice stems from the fact that historical returns for real estate and equity show a low correlation with each other. Real estate is notoriously stable, while equity carries high volatility in returns.

From the graph above, you may be thinking that the returns from the home price index appear dwarfed compared to the returns from equity in bull markets.

Please keep in mind that the home price index only measures the appreciation in the home’s price tag and doesn’t consider the annual rental returns over the holding period.

The weighted average returns from the S&P 500 stock index have a significant margin over treasury bonds or home prices during equity bull markets.

It is worth noting that the balance of stock and equity will generate the highest net returns during an equity bear market. The S&P 500 stock index takes a drastic nosedive into the negatives for returns in a bear market. In contrast, the home price index maintains a steadfast return and even performs better than during years with a bull equity market.

Balancing in equity and real estate would seem to be the natural optimal strategy to ward against negative returns in bear markets and capitalize on healthy returns for both equity and real estate in bull markets.

Investors still want to compare, and if you were to have only one choice, which would be the better option?

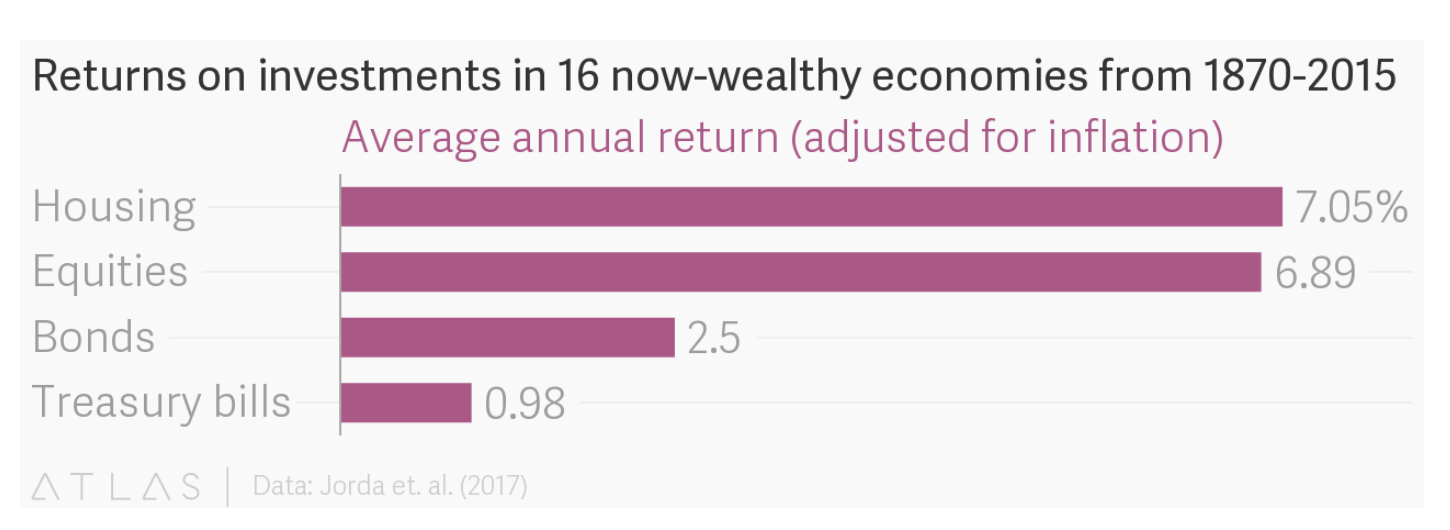

To truly compare the returns from different asset classes over prior periods, there isn’t anything as comprehensive as a data analysis report conducted by a team of economists from the University of California Davis, the University of Bonn, and the German Central Bank. (by Jorda et. al.)

This anchor report looks over data that spans 145 years from 1870 to 2015 for generalized categories of investment classes, including equity, residential real estate, short-term Treasury bills, and longer-term Treasury bonds.

So you know how we mentioned that the above chart doesn’t show annualized returns based on both appreciation and rental cash flow over the years for residential real estate?

Well, the research report aptly titled the Rate of Return on Everything, 1870-2015 measures and standardizes and measures the totality of returns of different asset classes by factoring in inflation, cash flows such as dividend or rent over the years, and the volatility of returns.

When looking at returns that include both period cash flows and price appreciation over the years, the returns from housing easily show as the clear winner, followed by equities, then bonds, then treasury bills.

Rental income proved an important factor—roughly half of the returns on real estate investments came from rental income, while the other half came from appreciation.

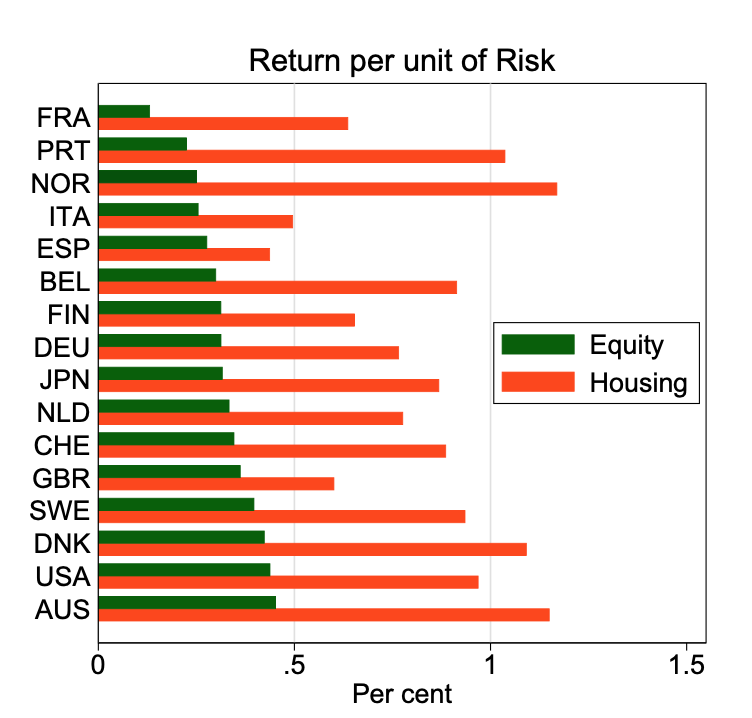

To take it one step further, because different investment asset classes carry different volatility and risk, the analysis report by Jorda et. al. (2017) evaluates risk-adjusted inflation-adjusted returns for asset classes.

A gold standard for measuring risk-adjusted returns, especially if you’re in the finance world, is the Sharpe ratio. This ratio divides excess returns from an asset class after taking out a risk-free rate as measured by returns from a Treasury bill by the standard deviation of returns, which is essentially a measure of the volatility of returns.

After accounting for equity and housing risk factors, the contrast between return measures for equity and housing shows even more starkly.

Housing provides a higher return per unit of risk in each of the 16 countries in the data sample and almost double that of equities.

A key hallmark of residential real estate is the ability to use financial leverage to magnify your returns. Financial leverage comes from being able to use financing from the bank to fund your investment in real estate. The concept is that you only need to put out very little personal capital and capitalize on bank financing to fund your purchase. During the holding period, rental cash flows from the property pay down your mortgage and increase your equity value in the property. This means that your costs of financing are covered by cash flows generated from the asset itself, and your returns are also coincidentally driven by corresponding increases in your equity stake. The ability to generate high returns while using minimal personal capital distinguishes real estate. In comparison, investing in stocks with debt, known as margin trading, is extremely risky and strictly for experienced traders.

In conclusion from this data research, you might be thinking, so why should I even bother with investing in equity?

Here are a few more practical elements to take into consideration :

The liquidity levels of real estate investing versus equity

Real estate is not an asset that you can trade from day-to-day, and the period for trade, i.e. your listing period before a home gets sold can be from a month to longer. In contrast, with equity, day trading is a common them when you’re looking to make small, but quick gains.

Your ability to diversify in the asset class

Real estate is an expensive asset and you are highly limited in your ability to invest in multiples of the asset. Because real estate values are highly reactive to local market conditions and real estate is immobile, it would be a nice-have to be able to invest in real estate in different communities to alleviate the risk if a certain local market should fall.

In contrast, having a low buy-in is what motivates most people to start out with investing in stocks. You can diversify across industries in stocks and even invest in REITs (Real estate Investment trusts) if you so choose.

Your level of involvement

With equity, your period returns which are made up of dividend distributions are entirely determined by the operational performance of a company, and you have no involvement.

If you want to generate rental returns from real estate investing you will need to exhibit some involvement even if you be outsourcing to a property management company. It is important to keep oversight over the kind of tenants being placed to stabilize rental cash flows, and you want to be careful and budget for all discriminate expenses for maintaining the property.

The Choice is Yours

In the end, the choice to invest in real estate or equity is purely discretionary and dependent on your own personal financial goals and needs. Either way, it is an important concept to look into investing in different investment classes to fund your future retirement or increase your personal wealth.

Would you like to connect with an expert and discuss how hot is the Real estate market? and where you should consider investing your money?